Overview

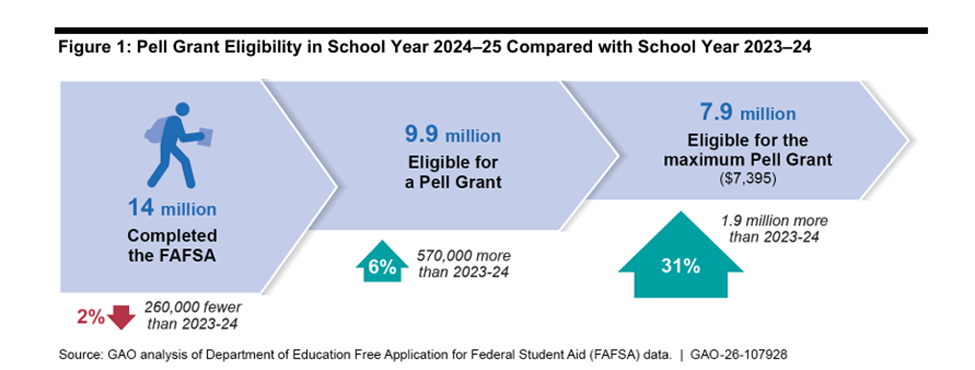

The US Government Accountability Office (GAO) recently released a comprehensive report of its analysis of federal data assessing how the FAFSA Simplification Act changed students' Pell Grant eligibility in 2024-25. The bottom line reinforces what we knew from the National College Attainment Network's (NCAN's) January analysis of data from the US Department of Education (ED): more than half a million more students became eligible for Pell, and almost two million more became eligible for the maximum award, even though fewer students completed the Free Application for Federal Student Aid (FAFSA) overall that year.

According to the GAO:

-

About 570,000 more students (6% more) were Pell-eligible in award year (AY) 2024–25 compared to AY 2023–24.

-

About 1.9 million more students (31% more) qualified for the maximum Pell award ($7,395).

-

The share of FAFSA completers who were Pell-eligible rose from 65% to 71%.

-

The average Pell award increased by $278, from $6,409 to $6,687.

What Changed in the Pell Formula?

Several formula changes drove the expansion of eligibility:

-

Higher income protection allowance (IPA) — More income is shielded from the aid calculation, resulting in more students qualifying for Pell Grants. FAFSA Simplification changed how the IPA is calculated by pegging it to the federal poverty level (150-400% based on family size and dependency status).

-

Raised asset reporting threshold — Families with income under $60,000 (up from $50,000 under the old formula) no longer need to report assets. FAFSA Simplification also included farm and small business assets in the calculation, but those changes were removed in the One Big Beautiful Bill Act (OBBBA) enacted last summer.

-

Automatic Pell eligibility — Students and parents with income at or below 175 -225% (determined by dependency and marital status) of the federal poverty level automatically qualify for the maximum Pell (currently $7,395); those up to 275–400% of the poverty level automatically qualify for the minimum Pell (currently $740).

-

Students in foster care and those experiencing homelessness are generally no longer required to re-verify their status every year. And students receiving nine federal safety net programs, such as Medicaid and SNAP, do not have to report their assets and are eligible to receive the Pell if they meet the relevant income threshold.

-

Incarcerated students, who were previously ineligible, are now eligible for Pell Grants once programs become approved by ED.

Who Gained the Most?

Middle-income families ($60K–$125K): At least 350,000 more students in the $60,001–$125,000 household income range became Pell-eligible when FAFSA Simplification went into effect, representing at least 61% of the total increase. The share of FAFSA completers in this range who were Pell-eligible jumped from 38% to at least 55%.

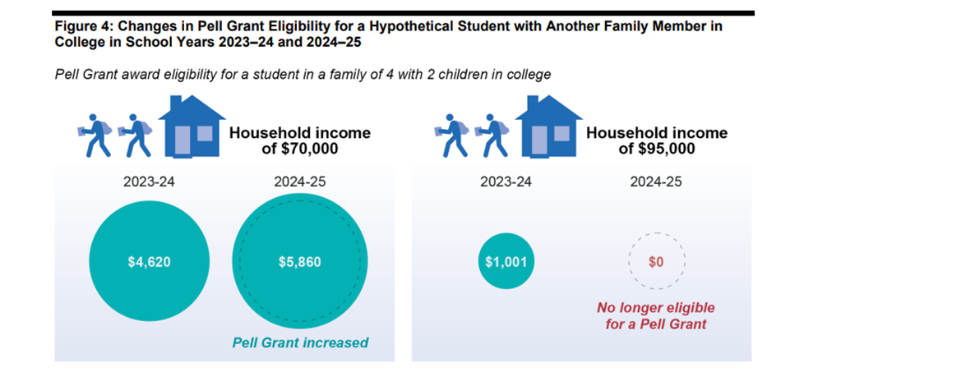

Families with multiple kids in college: 60% of students with at least one other family member in college were Pell-eligible in AY 2024–25 (up from 55%), and 77% of those were eligible for the maximum Pell (up sharply from 48%). This is notable because the "sibling discount" was removed from the formula when FAFSA Simplification was enacted. It turned out that other formula changes more than offset that loss for most families, however GAO flagged that some families in the $80K–$100K range who had previously benefited from the sibling discount may now be worse off.

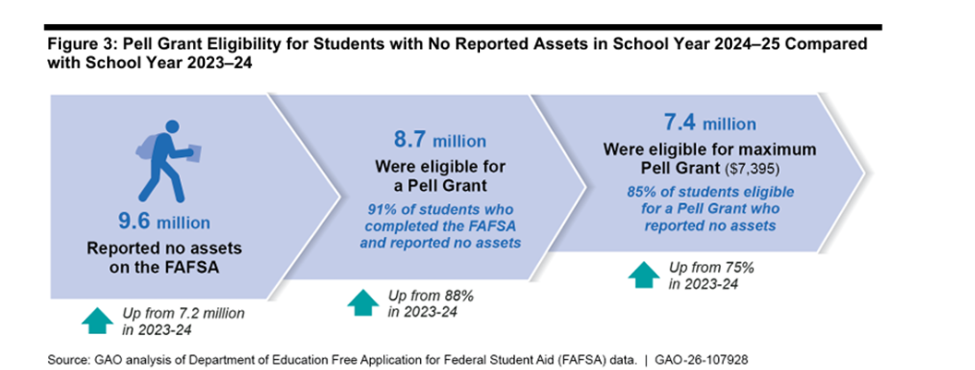

Students with no reported assets: About 2.4 million more students reported no assets in AY 2024–25, 91% percent of whom were Pell-eligible and 85% of whom qualified for the maximum Pell. Fewer families were required to report assets because of the higher threshold for asset reporting described above and the ability to qualify for a Pell Grant based on income and family size alone. This change benefitted many students from low-income families, but the GAO also reported that 37,000 students with assets over $500,000 were eligible for Pell Grants largely because they met the income test for a minimum or maximum Pell Grant, meaning they had high assets but low incomes. The OBBBA eliminated Pell eligibility for students with a Student Aid Index (SAI) that is twice the maximum Pell Grant. This change is likely to modestly reduce the number of Pell-eligible students, since the GAO noted that only 4% of students who completed the FAFSA and reported over $250,000 in assets were eligible for the maximum Pell.

Vulnerable populations: More than 90% of students in certain vulnerable populations, such as those who were homeless or in foster care, were Pell-eligible in AY 2024–25.

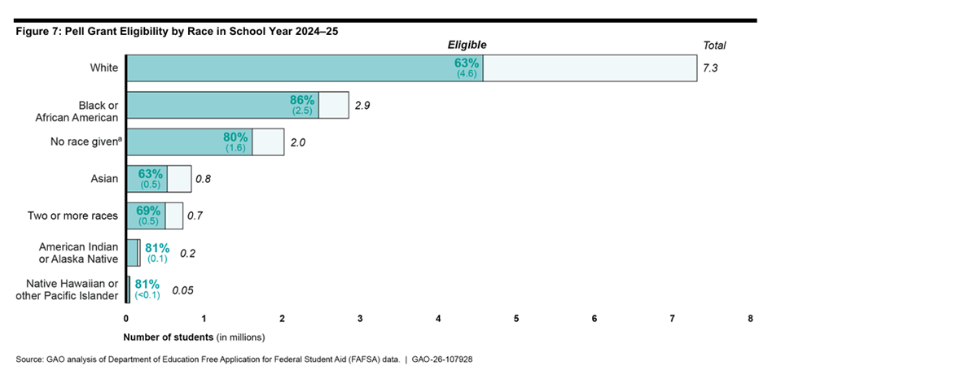

Pell Eligibility by Race and Ethnicity

FAFSA Simplification introduced demographic questions for the first time, and the GAO report gives us the first glimpse at how students responded. These questions were designed for research purposes only; they are not supposed to impact college admissions or financial aid decisions and are not sent to states, colleges, or universities. Students also had the option to decline to answer the questions, an option that may have been appealing to students in the wake of the US Supreme Court’s decision to strike down affirmative action. Some students of color expressed concern that they might face a backlash by schools afraid of being targeted for investigation by the Trump Administration.

The GAO reports that more than 86% of students answered the question about race, and 95% answered the question about ethnicity. Of those who provided their race, 86% of Black students were eligible for Pell Grants compared with 63% of white students. Eighty percent of students of Hispanic origin were eligible for Pell Grants compared with 67% of students who were not of Hispanic origin.

Because students were not required to answer questions about their race and ethnicity in prior years, we don’t have comparison data from previous years.

What College Access Advisors Should Know

-

For students at the margins of eligibility: Families earning between $60K–$125K who previously assumed they wouldn't qualify for Pell should be encouraged to complete the FAFSA and informed that they may be Pell-eligible. The new formula significantly expanded access at these income levels.

-

For families with siblings in college: Since most families with multiple children in college saw increased or maintained eligibility, advisors should work to dispel concerns about the removal of the “sibling discount.” While some families with higher incomes may have lost ground, most did not, and advisors should help families understand the likely benefit to them of the new formula.

-

For students with low incomes or who receive benefits: The automatic Pell eligibility tied to the federal poverty level is a meaningful protection that is helping many more students access Pell at any level, including the maximum Pell. With the maximum Pell Grant covering less than a third of the cost of attendance for an in-state student, and students overwhelmingly citing affordability as the key constraint on college-going, it’s meaningful to provide larger awards to more low-income students. Students receiving Medicaid, SNAP, TANF, SSI, or other means-tested benefits are more likely to qualify automatically, and the 2024–25 FAFSA expanded the list of programs from six to nine, resulting in more students being identified.

-

A caution about future years: AY 2024–25 may have been an atypical year as the first cycle under the new formula, and a time when the new FAFSA was still experiencing disruptions. Further, the OBBBA made additional changes to the eligibility formula for AY 2026–27 and beyond, including restoring small business and family farm asset exemptions, but also excluding students with high asset amounts from qualifying for Pell even if their income is low. Advisors should watch for updated guidance on how these changes play out in coming cycles.